I'd like to take a few minutes here to describe what are possibly the most dangerous of all financial contracts.. ones that Warren Buffet calls "financial weapons of mass destruction".. credit default swaps (CDS's). It was these devices that were a large part (but not the biggest part) of the financial meltdown last Sept.

A credit default swap is essentially an insurance policy on some investment you own.. for example, lets say you bought a Citibank corporate bond for $100,000. At some point, you (rightly) begin to get nervous about whether Citi will be able to pay you back. You therefore go to another big financial institution (small banks don't do this stuff) like AIG, which offers you insurance on your bond.. you pay AIG $2,000 a year and if the bond goes belly up, AIG will cough up the $100,000.

But wait.. it gets worse. Several very big companies like AIG began to underwrite CDS's on Citibank to people who did'nt even own Citibank bonds. It was, in other words, simply a bet. So... if Citibank went under, not only would they default on about $400 billion of loans to other banks, but another $400 billion would be lost by a number of companies like AIG who underwrote the CDS's on Citibank, for a total loss to the financial system of $800 billion-- thus making sure that if Citibank went under, AIG would then follow. This is exactly what happened to AIG.. they wrote about $100 billion of these policies on Lehman Brothers, and when Lehman went down, AIG went under the very next day since they only had like $23 billion in the bank. Whoops.

Then we get to the large companies that wrote CDS's on AIG.

It's called the domino effect. This is why last September's meltdown was so dangerous.

There has still been no regulation or banning of CDS's as of this writing.

CDS's are written by most big financial companies on nearly everything.. countries, cities, banks, mortgage bonds.. everything. When one big institution or city defaults, it unleashes a domino effect.

This is why the government bailed out all the banks, and it's why it will need to do so yet again in the not so distant future.

____________________________________________________________

The stock markets marched upward and onwards and the USD weakened a bit.. the exact opposite of what I needed for my "investment" (PSTIX) to appreciate.. it went from 5.55 down to 5.42; not a big loss, but not the direction I was hoping for. I need the stock markets to go down and the USD to appreciate for PSTIX to work well, and the S&P500 stubbornly refuses to cooperate, despite the reality back in the real world. Therefore I'm taking $2,500 from PSTIX and putting it into OCMGX, a metals fund, as gold continues it's march towards the stars.. this will be on a short leash, however. OCMGX is at 22.65 today, leaving $7,265 in PSTIX and the $2,500 in OCMGX.

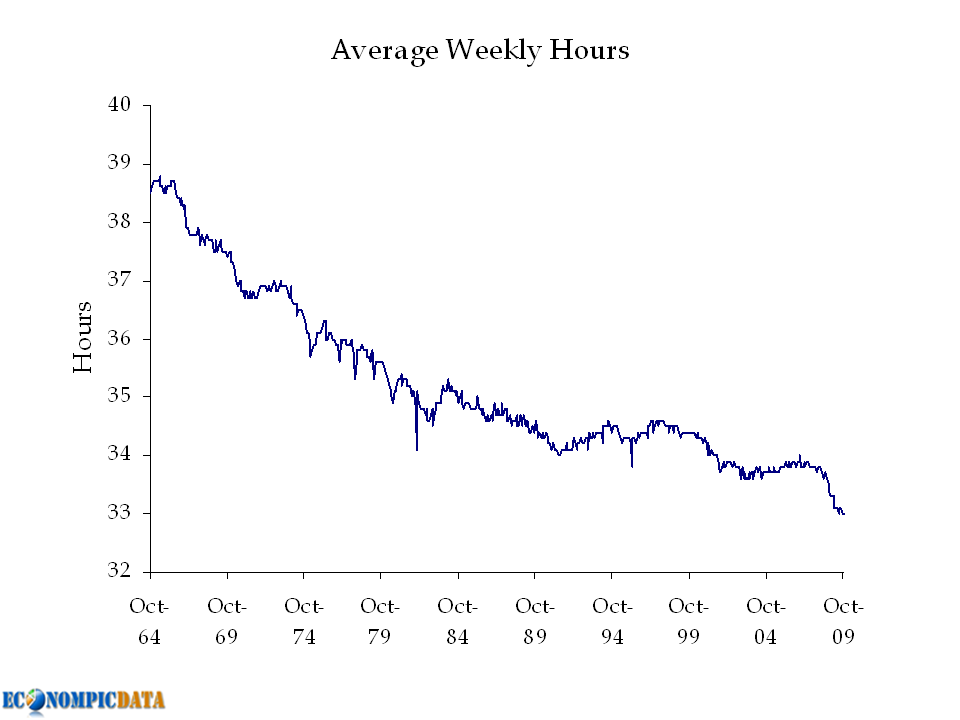

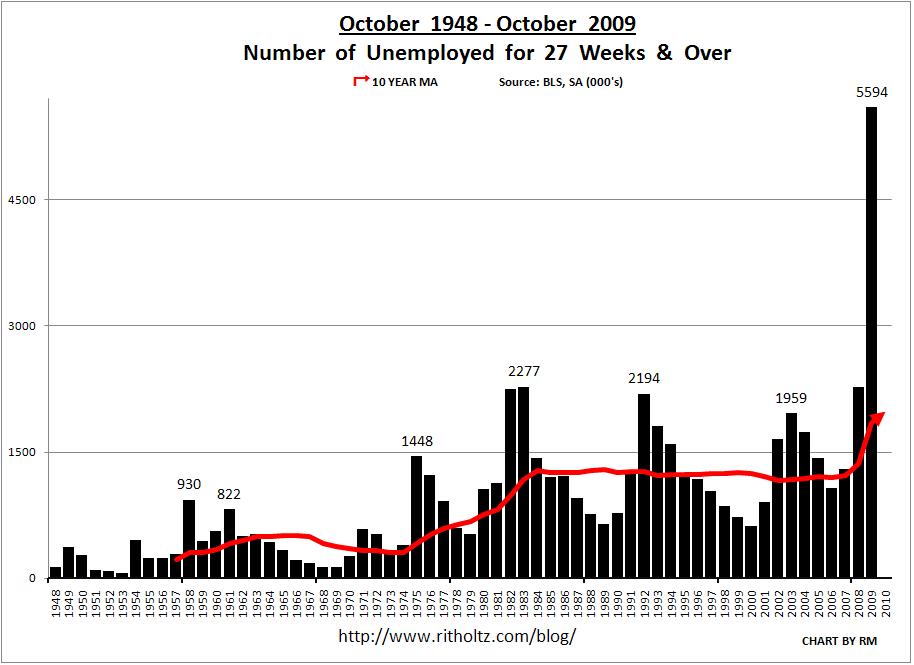

Back here in Hooverville, reality marches onwards... the unemployment report was worse than they expected.. another 200,000 jobs lost last month. Just 58.5% of adults are working, the lowest since 1983 (down from 63% 2 years ago). For those who don't know it, there are two unemployment measurements.. one called the U3 (which is where we get the current 10.2% figure) and the U6 (the old style count abandoned during the Clinton years) which went from 17.0% to 17.5%. Whats the difference ?? After six months of being unemployed, if you're still unemployed, it no longer counts as being unemployed.. you fall off as being a "discouraged worker". The U6 measurement includes these discouraged workers as well as those who can only get part time work. For me, it's the U6 number thats more accurate. I've included a few charts below showing not only the unemployment, but the shortening of hours worked/worker as well.. these are bad trends in an economy built upon consumer spending:

http://theautomaticearth.blogspot.com/2009/11/november-8-2009-jobs-doom-loop.html

http://www.ritholtz.com/blog/wp-content/uploads/2009/11/weekly_hours-worked-110609.png

http://www.ritholtz.com/blog/wp-content/uploads/2009/11/unemployment-october-1948-2009.JPG

There was a nugget of good news in there.. the gains in temp work. That is a leading indicator, though it must be said it's the holiday season and this might be a factor in temp hiring.

Next up on bloc is consumer credit.. this figure went down, and badly. However many dollars are being printed, they're not being lent out to you and me; as I alluded to earlier, they're sitting in bank vaults to cover bad loans. Worse, it appears to be accelerating as for the third quarter the rate of decline is 6%, but in September it was 7.25%. This should strengthen the USD (and my PSTIX) Here's todays numbers:

"Consumer credit decreased at an annual rate of 6 percent in the third quarter of 2009. Revolving credit decreased at an annual rate of 10 percent, and nonrevolving credit decreased at an annual rate of 3-3/4 percent. In September, consumer credit decreased at an annual rate of 7-1/4 percent"

http://market-ticker.denninger.net/uploads/Nov2009/credit.png

Remember, the US economy is 70% consumption.. and if people are not working, if those who are working are working less hours, and they have less and less available credit, who will do the consuming ?? This is Exhibit A on why I believe all is not well, why I think a bout of deflation is coming, and behind it all is the mountain of debt we're still in, a decent part of which is guaranteed by the taxpayers. I caught this little blurb on the article which says Freddie Mac lost another $5 billion last month:

"Starting in 2010, Freddie Mac will begin accounting for $1.8 trillion in mortgage-backed securities it guarantees on its balance sheet to meet new guidelines. This will increase interest income and interest expenses, and could have a significant negative impact on net worth, it said"

Who backs up Freddie Mac and that $1.8 trillion ?? Yep.. us taxpayers. It's "heads I win, tails you lose" in the housing markets these days.

CitiGroup is (again) in trouble, and with the rumblings in Wash DC to break up the "too big to fails", I'm beginning to think that Citi might be the first patient on the operating table. There are parts of Citi that are gems.. but as a whole, they went so deep into subprime mortgages that overall it's toast:

http://www.nytimes.com/2009/11/01/business/economy/01citi.html

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment