Well another banner day.. copper opened at $3.1325 with a high of $3.184.. so again I made another $1,000 today as my order was to "buy" at $3.14 and sell at $3.18. I'm beginning to like this copper thing !! The day ended at $3.17ish. Not sure where we're goin from here; copper has problems breaking thru $3.19, but we are still in a bull market... I'm going to put in an order to "buy" March copper @ $3.20 with a three cent trailing stop and a goal of $3.24. This brings my imaginary account to $13,027.

Apparently the Japanese prime minister and the governor of the Bank of Japan have heard my cries.. dare I say they're followers of my humble blog ??

"TOKYO (Dow Jones)--Japan's top government spokesman said he expects Prime Minister Yukio Hatoyama and Bank of Japan Gov. Masaaki Shirakawa to exchange opinions on the economy and to discuss the possibility of the central bank adopting a policy of quantitative easing, local media reported Monday"

Monday, November 30, 2009

Saturday, November 28, 2009

Update 11/28

A minor panic happened on Thanksgiving Day and yesterday as the tiny oilpit Dubai threatened to default on about $80 billion of debt, mostly to EU and Japanese banks. Barclays and RBS especially took it on the chops. Me thinks this is a small matter and monday we'll be back to the same old story.. stock markets & metals going up and up. Therefore I'm putting in an order to "buy" March '10 copper again $3.14 Monday morning with a goal of $3.18 (copper is @ $3.105 now) with a two cent trailing stop.. same play as last week. I'll also be looking to "sell" copper at $3.00 with a two cent stop should it go that low.

In a tad more ominous news, the Yen streaked up to 118 (a major move) versus the dollar on the overnight market before the BOJ intervened and bought dollars. There is a very real and growing chance that Japan will be in a seriously deflationary state soon enough. The BOJ must do something, and before year's end I think they will.

In a tad more ominous news, the Yen streaked up to 118 (a major move) versus the dollar on the overnight market before the BOJ intervened and bought dollars. There is a very real and growing chance that Japan will be in a seriously deflationary state soon enough. The BOJ must do something, and before year's end I think they will.

Wednesday, November 25, 2009

Update 11/25

Well today was a wild one.. I "bought" a copper contract at $3.14 and bailed at $3.18 for a dandy profit of $1,000 just today. Wow !! Copper opened at $3.135 and went all the way up to $3.184 today.. quite the move. The USD tanked; gold shot up as well. Crude also gained a couple dollars to close above $78/bbl. Now that's the way to begin the holidays !! This brings my imaginary account up to $12,027.

Monday, November 23, 2009

Update 11/23

Both gold and copper shot up this morning, then pulled back and finished near the session lows, with another pullback likely coming tomorrow mornin, and all this despite the USD falling again. So, I'm going to pull out of both OCMGX and my copper contract... OCGMX wound up at 24.79, for a profit of $223 and my copper closed at 3.125, for a profit of $437.50, bringing my total up to $11,027.50. I'm going to put in the order to "buy" copper again if it gets to $3.14, with a goal of $3.18 and a trailing stop of two cents just in case this is just a one day pullback. I'll "sell" any drop below $3.00

Friday, November 20, 2009

Update 11/20

My OCMGX wound up at 24.28 today, up from 23.81 last week, for a gain of $145, bringing my total to $10,367. For at least two days this week (including today) the USDX went up, which should've made gold go lower. Instead it went up, which to me is a sign of gold's bullish intentions and a basic theory that the USD might rise or sink versus other currencies, but as so many of them are being printed, the USD is sinking in relation to commodities, gold in particular. So for

the meantime, I'm sticking by my OCMGX.. more or less. I'm going to remove $4,000 and move into the commodities market, "buying" a Dec 09 copper contract at today's close price of $3.107. This is a contract for 25,000 lb of copper.. for every cent the price goes up, I'll make $250.. and for every cent it goes down.. well, we won't talk about that. I've got a trailing stop on it of three cents; I will exit this if copper hits 3.20 or at the end of next week, whichever comes first.

I'm beginning to think that a market pullback is coming, and with this would be a rising USD. Next week will be very telling; I'm going to keep on my toes and see if there is a clear diretion. The deflation bug seems to be in the air.

Nothing dramatic happened this week; the housing market came out with some fugly numbers, but still the markets rallied. At some point, if the fundamentals on the ground don't begin to improve, the stock markets will need to come back down. Lets hope this is the beginning of a recovery and that the fundamentals out here in Hooverville begin to get better.

Meredith Whitney came out this week and said that since the stock market highs last year, there has been $1.5 trillion of available credit removed from the consumers, and she went on to say that another $1.2 trillion more will evaporate. This has, and will, continue to hamper consumer spending. http://www.calculatedriskblog.com/2009/11/fed-and-mortgage-rates.html

Something wierd happened last nite on the ICE exchange overnight markets.. there was a huge buy order on the USDX that would've sent the USDX from 76.5 to over 80.. a pretty dramatic move. The ICE exchange decided to simply void the order.. some 4,000 contracts. Apparently this happened earlier this month as well, that time to the tune of 8,000 contracts: http://www.zerohedge.com/article/were-you-affected-todays-ice-dxy-order-cancellation-let-us-know

the meantime, I'm sticking by my OCMGX.. more or less. I'm going to remove $4,000 and move into the commodities market, "buying" a Dec 09 copper contract at today's close price of $3.107. This is a contract for 25,000 lb of copper.. for every cent the price goes up, I'll make $250.. and for every cent it goes down.. well, we won't talk about that. I've got a trailing stop on it of three cents; I will exit this if copper hits 3.20 or at the end of next week, whichever comes first.

I'm beginning to think that a market pullback is coming, and with this would be a rising USD. Next week will be very telling; I'm going to keep on my toes and see if there is a clear diretion. The deflation bug seems to be in the air.

Nothing dramatic happened this week; the housing market came out with some fugly numbers, but still the markets rallied. At some point, if the fundamentals on the ground don't begin to improve, the stock markets will need to come back down. Lets hope this is the beginning of a recovery and that the fundamentals out here in Hooverville begin to get better.

Meredith Whitney came out this week and said that since the stock market highs last year, there has been $1.5 trillion of available credit removed from the consumers, and she went on to say that another $1.2 trillion more will evaporate. This has, and will, continue to hamper consumer spending. http://www.calculatedriskblog.com/2009/11/fed-and-mortgage-rates.html

Something wierd happened last nite on the ICE exchange overnight markets.. there was a huge buy order on the USDX that would've sent the USDX from 76.5 to over 80.. a pretty dramatic move. The ICE exchange decided to simply void the order.. some 4,000 contracts. Apparently this happened earlier this month as well, that time to the tune of 8,000 contracts: http://www.zerohedge.com/article/were-you-affected-todays-ice-dxy-order-cancellation-let-us-know

Tuesday, November 17, 2009

The Carry Trade

In about 1995, the Bank of Japan lowered their interest rates to nearly zero. This invited investors to borrow from the BOJ since it was so cheap. Investors borrowing at low interest rates in yen used the loan to buy higher yielding assets elsewhere. Perhaps the most popular form of the strategy exploited the gap between US and Japanese yields. Anyone borrowing for next to nothing in yen, convert it into US dollars, and putting the money into US Treasuries (US government bonds) paying 3 1/2% got a double pay-off: from an interest rate difference of more than three percentage points and from the dollar’s rise against the yen (when they reversed the trade and paid back the yen loan, they needed to re-convert USD into yen.. and by the time this happened, the yen had fallen even further). It was called the "Yen Carry Trade".

When the yen began to appreciate (in about 2006 the BOJ began hiking rates), those investors had to pay back those loans with more interest.. and so they began to repay ASAP in order to get the lowest payback possible as the BOJ raised rates again and again. By then, the yen was also badly undervalued, and forex speculators "bought" the yen. As the exchange rate of yen vs other currencies went up (very quickly), the second part of their scheme also went to pot and those investors then took yet more losses on the re-conversion from the local currencies back into yen. The yen went from 8,200 in mid-2007 to around 11,500 by the end of 2008: http://futures.tradingcharts.com/chart/JY/M

This flood of cheap money also helped in large part to fuel the speculative bubble in Asia in the mid-1990's; investors would borrow from the BOJ, convert it to the local currency (thus making the local currency go up in value) and invest it in their stock markets & real estate. These nations' stock markets & currencies rose to unrealistic levels, with predictable results. Worse, as their currencies went south, their governments had to borrow money at higher interest rates to make up for the collapsing currency value. Thus came the Asian Economic Crisis of 1997, with the IMF needing to bail out Korea, Thailand and a few others.

Here we are in 2009.. and this time, it's the US that has drastically lowered interest rates. This carry trade is large part of why the US dollar is sinking (investors are selling USD and buying other currencies to invest in those nations.). It's also part of the reason why our own stock markets are going up and why Bonds have not had a particularly difficult time finding investors. Here's an article from Hong Kong's governor, who also saw the 1997 debacle, on the Dollar Carry Trade: http://www.bloomberg.com/apps/news?pid=20601068&sid=aU3AiTc_Q_vk

The danger here is the same as with the yen trade.. that at some point, the USD could rebound violently, with profound repurcussions. This is a video from Nouriel Roubini, one of the few economists who saw last year's crisis, on the Dollar Carry Trade: http://www.youtube.com/watch?v=xIEoa3F5o0M

It's just these types of currency games that make small problems into very dangerous ones.

When the yen began to appreciate (in about 2006 the BOJ began hiking rates), those investors had to pay back those loans with more interest.. and so they began to repay ASAP in order to get the lowest payback possible as the BOJ raised rates again and again. By then, the yen was also badly undervalued, and forex speculators "bought" the yen. As the exchange rate of yen vs other currencies went up (very quickly), the second part of their scheme also went to pot and those investors then took yet more losses on the re-conversion from the local currencies back into yen. The yen went from 8,200 in mid-2007 to around 11,500 by the end of 2008: http://futures.tradingcharts.com/chart/JY/M

This flood of cheap money also helped in large part to fuel the speculative bubble in Asia in the mid-1990's; investors would borrow from the BOJ, convert it to the local currency (thus making the local currency go up in value) and invest it in their stock markets & real estate. These nations' stock markets & currencies rose to unrealistic levels, with predictable results. Worse, as their currencies went south, their governments had to borrow money at higher interest rates to make up for the collapsing currency value. Thus came the Asian Economic Crisis of 1997, with the IMF needing to bail out Korea, Thailand and a few others.

Here we are in 2009.. and this time, it's the US that has drastically lowered interest rates. This carry trade is large part of why the US dollar is sinking (investors are selling USD and buying other currencies to invest in those nations.). It's also part of the reason why our own stock markets are going up and why Bonds have not had a particularly difficult time finding investors. Here's an article from Hong Kong's governor, who also saw the 1997 debacle, on the Dollar Carry Trade: http://www.bloomberg.com/apps/news?pid=20601068&sid=aU3AiTc_Q_vk

The danger here is the same as with the yen trade.. that at some point, the USD could rebound violently, with profound repurcussions. This is a video from Nouriel Roubini, one of the few economists who saw last year's crisis, on the Dollar Carry Trade: http://www.youtube.com/watch?v=xIEoa3F5o0M

It's just these types of currency games that make small problems into very dangerous ones.

Sunday, November 15, 2009

Beggar Thy Neighbor

During the Depression, America and Britain became desperate to sell their goods overseas, and so they put up trade barriers so other nations could'nt realistically sell their goods here and they lowered the value of their currencies to make their own exports cheaper; it was a good attempt at trying to export their way out of the Depression. The problem was, other nations followed suit, and there was a huge drop in trade, making the Depression much worse than it needed to be. These policies became known as "beggar thy neighbor".

When a nation's currency goes down in value, they are able to export more because their goods cost less versus a nation's goods who's currency is worth quite a bit. China has achieved a large trade surplus for a good decade (in part) at least because they have held down the value of their currency relative to other currencies.

Currently, the US is printing money like madmen, lowering the cost of our exports. China has kept up the pace for the most part. But for other nations: Japan, Brazil, Euroland.. it has meant that their exports have become more expensive and their exports are beginning to suffer. Here is a chart of the Brazilian currency, the Real: http://futuresource.quote.com/charts/charts.jsp?s=QBR%20Z9 and here is a chart of the US Dollar: http://futuresource.quote.com/charts/charts.jsp?s=DX%20Z9. Here the Brazilian currency has appreciated nearly 50% in the last six months, making their exports much more expensive versus American exports simply because of currency manipulations.

President Obama is currently in China for talks with their leaders; we are pushing for them to raise the value of their currency; they are doing the same with us. Obama was also in Tokyo, where the discussion was much the same, though the Yen has been rising for much of the year.

The danger is that other nations (especially Japan) will begin to crank up the printing presses as well. The Japanese Gov't will need to borrow $500 billion next year, and their savings rate is at 2%, half what it is in America... in other words, the Japanese people are tapped out. For them to borrow that much money (probably half the total) from other nations is a stretch, and their interest rates could concievably rise to attract these foreign buyers. What to do ?? Copy Ben Bernanke, who printed up nearly half a trillion dollar bills and "bought" US Gov't bonds.

And herein lies the problem.. at some point, it might become a race to the bottom. As money printing increases, the price we all pay for basic goods increases, though so far this has not yet happened as most of the printed money has found its way into the stock market and bank vaults. Disturbingly, the CRB index (which measures a broad range of commodities) has gone up, possibly portending inflation: http://quotes.ino.com/chart/?s=NYBOT_CR&v=d12. If inflation did begin in the US and goods did become more expensive, don't expect employers to automatically start giving raises. Back in Hooverville, our standard of living will simply decline.

The world economy is still skating on thin ice, and dangerous currency games are the last thing anybody needs.

When a nation's currency goes down in value, they are able to export more because their goods cost less versus a nation's goods who's currency is worth quite a bit. China has achieved a large trade surplus for a good decade (in part) at least because they have held down the value of their currency relative to other currencies.

Currently, the US is printing money like madmen, lowering the cost of our exports. China has kept up the pace for the most part. But for other nations: Japan, Brazil, Euroland.. it has meant that their exports have become more expensive and their exports are beginning to suffer. Here is a chart of the Brazilian currency, the Real: http://futuresource.quote.com/charts/charts.jsp?s=QBR%20Z9 and here is a chart of the US Dollar: http://futuresource.quote.com/charts/charts.jsp?s=DX%20Z9. Here the Brazilian currency has appreciated nearly 50% in the last six months, making their exports much more expensive versus American exports simply because of currency manipulations.

President Obama is currently in China for talks with their leaders; we are pushing for them to raise the value of their currency; they are doing the same with us. Obama was also in Tokyo, where the discussion was much the same, though the Yen has been rising for much of the year.

The danger is that other nations (especially Japan) will begin to crank up the printing presses as well. The Japanese Gov't will need to borrow $500 billion next year, and their savings rate is at 2%, half what it is in America... in other words, the Japanese people are tapped out. For them to borrow that much money (probably half the total) from other nations is a stretch, and their interest rates could concievably rise to attract these foreign buyers. What to do ?? Copy Ben Bernanke, who printed up nearly half a trillion dollar bills and "bought" US Gov't bonds.

And herein lies the problem.. at some point, it might become a race to the bottom. As money printing increases, the price we all pay for basic goods increases, though so far this has not yet happened as most of the printed money has found its way into the stock market and bank vaults. Disturbingly, the CRB index (which measures a broad range of commodities) has gone up, possibly portending inflation: http://quotes.ino.com/chart/?s=NYBOT_CR&v=d12. If inflation did begin in the US and goods did become more expensive, don't expect employers to automatically start giving raises. Back in Hooverville, our standard of living will simply decline.

The world economy is still skating on thin ice, and dangerous currency games are the last thing anybody needs.

Friday, November 13, 2009

Update 11/13

OCMGX wound up the week at 23.81, for a profit of $497 this week on my gold play, bringing my imaginary account to $10,222. Given that there is absolutely no sign from the Fed that they'll stop printing, and an article in the Telegraph that world gold production is in decline, me thinks I'll just sit and profit for the time being, though I must say I think a small pull back might be in the cards.

On the muni bond front came this: "In California's latest offering-- a sale Tuesday of $1.9 billion in bonds maturing in June 2013-- the state had to pony up 4% annualized tax-free yield to lure investors to the deal. Less than two weeks ago, the state paid a yield of 2.48% on a bond with a similar maturity" http://latimesblogs.latimes.com/money_co/2009/11/california-muni-bond-sale-tax-free-market-yields.html That is a really bad sign for the Governator.

This article is a good treatise on the chances of bond defaults by the seven biggest economies in the world, rating which one is the most likely to default.. and the (well) winner is.. http://www.prudentbear.com/index.php/thebearslairview?art_id=10307

Nothing too earth shattering this week, just more of the same.. stock markets & gold up, more unemployment and misery in Hooverville. At some point either the markets will sink... or... life in Hooverville will get better, but right now there is a serious disconnect between the party on Wall Street and the misery on Main Street.

On the muni bond front came this: "In California's latest offering-- a sale Tuesday of $1.9 billion in bonds maturing in June 2013-- the state had to pony up 4% annualized tax-free yield to lure investors to the deal. Less than two weeks ago, the state paid a yield of 2.48% on a bond with a similar maturity" http://latimesblogs.latimes.com/money_co/2009/11/california-muni-bond-sale-tax-free-market-yields.html That is a really bad sign for the Governator.

This article is a good treatise on the chances of bond defaults by the seven biggest economies in the world, rating which one is the most likely to default.. and the (well) winner is.. http://www.prudentbear.com/index.php/thebearslairview?art_id=10307

Nothing too earth shattering this week, just more of the same.. stock markets & gold up, more unemployment and misery in Hooverville. At some point either the markets will sink... or... life in Hooverville will get better, but right now there is a serious disconnect between the party on Wall Street and the misery on Main Street.

Monday, November 9, 2009

Update 11/9

Have decided to bail out of PSTIX and am going all in for the gold fund OCMGX (today at 22.65) for a total of $9,725 in OCMGX. The DOW and Gold simply want to go to the moon.

At the recent G20 meeting, the verdict in regards to the US Dollar (with our shameful leaders in agreement) is "let it sink like an boulder off a cliff". The "carry trade" is whats lifting the stock market, and Bernanke has apparently said this will continue until the unemployment rate begins to drop again, and this could be quite a while.

The overall trends here seem to be that all this money being printed is going one of two places: the stock markets and the US bond markets, neither of which have any trouble attracting huge amounts of money. But for the rest of us in Hooverville, the availability of cash is actually headed south as indicated by last week's consumer credit numbers; economist David Rosenberg says that 1/5th of all consumer credit is gone on a permanent basis so far. Worse, the value of the dollar versus crude oil is going down, making basic goods more and more expensive at a time when unemployment is rising and available credit is sinking.

There is a consequence to this, and that consequence will be inflation.. by year's end I can see gas hitting $3.00/gal and if this continues unabated, will near $4.00/gal next summer. Food (which is transported by truck in most cases) will also go up in price. Worse, I honestly think the Obama Administration could care less (because of environmental reasons) if gas hits $4.00/gal. But they should care for economic reasons; this means consumers will have less to spend and to pay bills with, affecting retail stores and loan default rates.

Once again, this is going to end very badly.

At the recent G20 meeting, the verdict in regards to the US Dollar (with our shameful leaders in agreement) is "let it sink like an boulder off a cliff". The "carry trade" is whats lifting the stock market, and Bernanke has apparently said this will continue until the unemployment rate begins to drop again, and this could be quite a while.

The overall trends here seem to be that all this money being printed is going one of two places: the stock markets and the US bond markets, neither of which have any trouble attracting huge amounts of money. But for the rest of us in Hooverville, the availability of cash is actually headed south as indicated by last week's consumer credit numbers; economist David Rosenberg says that 1/5th of all consumer credit is gone on a permanent basis so far. Worse, the value of the dollar versus crude oil is going down, making basic goods more and more expensive at a time when unemployment is rising and available credit is sinking.

There is a consequence to this, and that consequence will be inflation.. by year's end I can see gas hitting $3.00/gal and if this continues unabated, will near $4.00/gal next summer. Food (which is transported by truck in most cases) will also go up in price. Worse, I honestly think the Obama Administration could care less (because of environmental reasons) if gas hits $4.00/gal. But they should care for economic reasons; this means consumers will have less to spend and to pay bills with, affecting retail stores and loan default rates.

Once again, this is going to end very badly.

Saturday, November 7, 2009

Credit Default Swaps & update

I'd like to take a few minutes here to describe what are possibly the most dangerous of all financial contracts.. ones that Warren Buffet calls "financial weapons of mass destruction".. credit default swaps (CDS's). It was these devices that were a large part (but not the biggest part) of the financial meltdown last Sept.

A credit default swap is essentially an insurance policy on some investment you own.. for example, lets say you bought a Citibank corporate bond for $100,000. At some point, you (rightly) begin to get nervous about whether Citi will be able to pay you back. You therefore go to another big financial institution (small banks don't do this stuff) like AIG, which offers you insurance on your bond.. you pay AIG $2,000 a year and if the bond goes belly up, AIG will cough up the $100,000.

But wait.. it gets worse. Several very big companies like AIG began to underwrite CDS's on Citibank to people who did'nt even own Citibank bonds. It was, in other words, simply a bet. So... if Citibank went under, not only would they default on about $400 billion of loans to other banks, but another $400 billion would be lost by a number of companies like AIG who underwrote the CDS's on Citibank, for a total loss to the financial system of $800 billion-- thus making sure that if Citibank went under, AIG would then follow. This is exactly what happened to AIG.. they wrote about $100 billion of these policies on Lehman Brothers, and when Lehman went down, AIG went under the very next day since they only had like $23 billion in the bank. Whoops.

Then we get to the large companies that wrote CDS's on AIG.

It's called the domino effect. This is why last September's meltdown was so dangerous.

There has still been no regulation or banning of CDS's as of this writing.

CDS's are written by most big financial companies on nearly everything.. countries, cities, banks, mortgage bonds.. everything. When one big institution or city defaults, it unleashes a domino effect.

This is why the government bailed out all the banks, and it's why it will need to do so yet again in the not so distant future.

____________________________________________________________

The stock markets marched upward and onwards and the USD weakened a bit.. the exact opposite of what I needed for my "investment" (PSTIX) to appreciate.. it went from 5.55 down to 5.42; not a big loss, but not the direction I was hoping for. I need the stock markets to go down and the USD to appreciate for PSTIX to work well, and the S&P500 stubbornly refuses to cooperate, despite the reality back in the real world. Therefore I'm taking $2,500 from PSTIX and putting it into OCMGX, a metals fund, as gold continues it's march towards the stars.. this will be on a short leash, however. OCMGX is at 22.65 today, leaving $7,265 in PSTIX and the $2,500 in OCMGX.

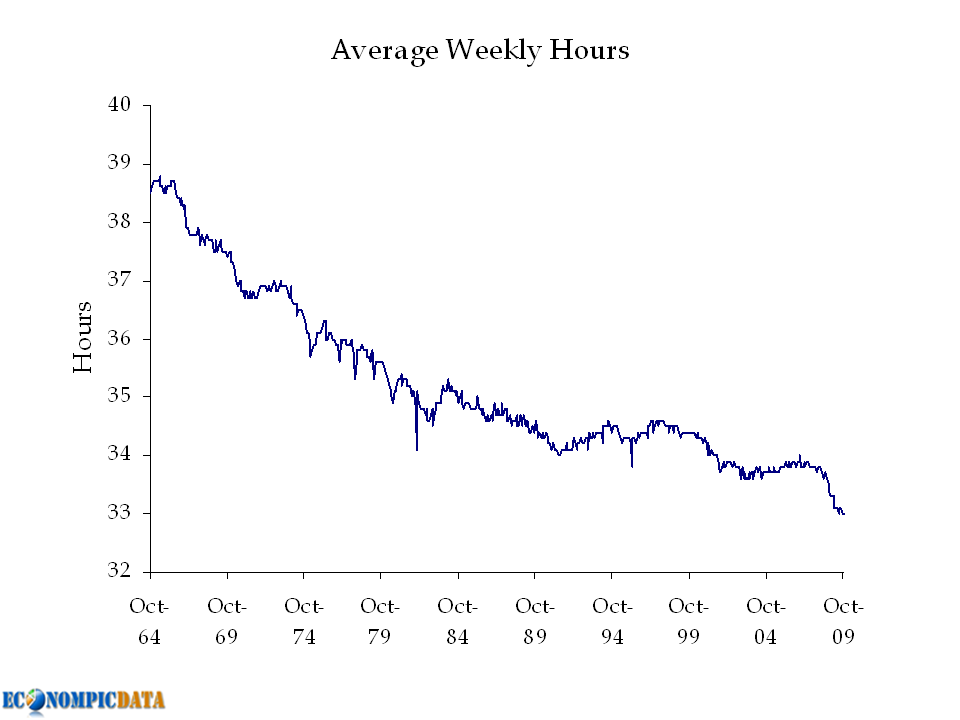

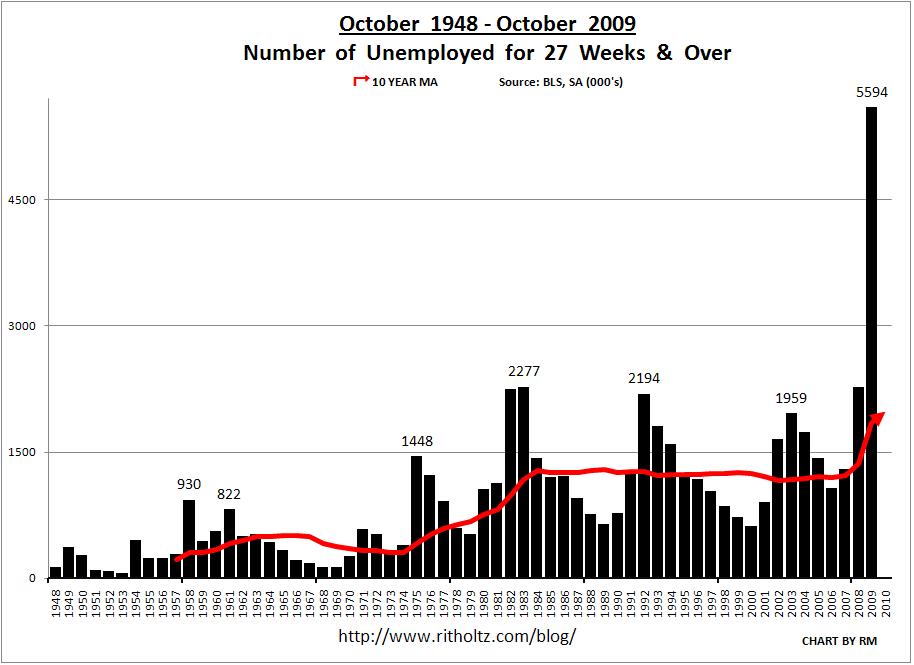

Back here in Hooverville, reality marches onwards... the unemployment report was worse than they expected.. another 200,000 jobs lost last month. Just 58.5% of adults are working, the lowest since 1983 (down from 63% 2 years ago). For those who don't know it, there are two unemployment measurements.. one called the U3 (which is where we get the current 10.2% figure) and the U6 (the old style count abandoned during the Clinton years) which went from 17.0% to 17.5%. Whats the difference ?? After six months of being unemployed, if you're still unemployed, it no longer counts as being unemployed.. you fall off as being a "discouraged worker". The U6 measurement includes these discouraged workers as well as those who can only get part time work. For me, it's the U6 number thats more accurate. I've included a few charts below showing not only the unemployment, but the shortening of hours worked/worker as well.. these are bad trends in an economy built upon consumer spending:

http://theautomaticearth.blogspot.com/2009/11/november-8-2009-jobs-doom-loop.html

http://www.ritholtz.com/blog/wp-content/uploads/2009/11/weekly_hours-worked-110609.png

http://www.ritholtz.com/blog/wp-content/uploads/2009/11/unemployment-october-1948-2009.JPG

There was a nugget of good news in there.. the gains in temp work. That is a leading indicator, though it must be said it's the holiday season and this might be a factor in temp hiring.

Next up on bloc is consumer credit.. this figure went down, and badly. However many dollars are being printed, they're not being lent out to you and me; as I alluded to earlier, they're sitting in bank vaults to cover bad loans. Worse, it appears to be accelerating as for the third quarter the rate of decline is 6%, but in September it was 7.25%. This should strengthen the USD (and my PSTIX) Here's todays numbers:

"Consumer credit decreased at an annual rate of 6 percent in the third quarter of 2009. Revolving credit decreased at an annual rate of 10 percent, and nonrevolving credit decreased at an annual rate of 3-3/4 percent. In September, consumer credit decreased at an annual rate of 7-1/4 percent"

http://market-ticker.denninger.net/uploads/Nov2009/credit.png

Remember, the US economy is 70% consumption.. and if people are not working, if those who are working are working less hours, and they have less and less available credit, who will do the consuming ?? This is Exhibit A on why I believe all is not well, why I think a bout of deflation is coming, and behind it all is the mountain of debt we're still in, a decent part of which is guaranteed by the taxpayers. I caught this little blurb on the article which says Freddie Mac lost another $5 billion last month:

"Starting in 2010, Freddie Mac will begin accounting for $1.8 trillion in mortgage-backed securities it guarantees on its balance sheet to meet new guidelines. This will increase interest income and interest expenses, and could have a significant negative impact on net worth, it said"

Who backs up Freddie Mac and that $1.8 trillion ?? Yep.. us taxpayers. It's "heads I win, tails you lose" in the housing markets these days.

CitiGroup is (again) in trouble, and with the rumblings in Wash DC to break up the "too big to fails", I'm beginning to think that Citi might be the first patient on the operating table. There are parts of Citi that are gems.. but as a whole, they went so deep into subprime mortgages that overall it's toast:

http://www.nytimes.com/2009/11/01/business/economy/01citi.html

A credit default swap is essentially an insurance policy on some investment you own.. for example, lets say you bought a Citibank corporate bond for $100,000. At some point, you (rightly) begin to get nervous about whether Citi will be able to pay you back. You therefore go to another big financial institution (small banks don't do this stuff) like AIG, which offers you insurance on your bond.. you pay AIG $2,000 a year and if the bond goes belly up, AIG will cough up the $100,000.

But wait.. it gets worse. Several very big companies like AIG began to underwrite CDS's on Citibank to people who did'nt even own Citibank bonds. It was, in other words, simply a bet. So... if Citibank went under, not only would they default on about $400 billion of loans to other banks, but another $400 billion would be lost by a number of companies like AIG who underwrote the CDS's on Citibank, for a total loss to the financial system of $800 billion-- thus making sure that if Citibank went under, AIG would then follow. This is exactly what happened to AIG.. they wrote about $100 billion of these policies on Lehman Brothers, and when Lehman went down, AIG went under the very next day since they only had like $23 billion in the bank. Whoops.

Then we get to the large companies that wrote CDS's on AIG.

It's called the domino effect. This is why last September's meltdown was so dangerous.

There has still been no regulation or banning of CDS's as of this writing.

CDS's are written by most big financial companies on nearly everything.. countries, cities, banks, mortgage bonds.. everything. When one big institution or city defaults, it unleashes a domino effect.

This is why the government bailed out all the banks, and it's why it will need to do so yet again in the not so distant future.

____________________________________________________________

The stock markets marched upward and onwards and the USD weakened a bit.. the exact opposite of what I needed for my "investment" (PSTIX) to appreciate.. it went from 5.55 down to 5.42; not a big loss, but not the direction I was hoping for. I need the stock markets to go down and the USD to appreciate for PSTIX to work well, and the S&P500 stubbornly refuses to cooperate, despite the reality back in the real world. Therefore I'm taking $2,500 from PSTIX and putting it into OCMGX, a metals fund, as gold continues it's march towards the stars.. this will be on a short leash, however. OCMGX is at 22.65 today, leaving $7,265 in PSTIX and the $2,500 in OCMGX.

Back here in Hooverville, reality marches onwards... the unemployment report was worse than they expected.. another 200,000 jobs lost last month. Just 58.5% of adults are working, the lowest since 1983 (down from 63% 2 years ago). For those who don't know it, there are two unemployment measurements.. one called the U3 (which is where we get the current 10.2% figure) and the U6 (the old style count abandoned during the Clinton years) which went from 17.0% to 17.5%. Whats the difference ?? After six months of being unemployed, if you're still unemployed, it no longer counts as being unemployed.. you fall off as being a "discouraged worker". The U6 measurement includes these discouraged workers as well as those who can only get part time work. For me, it's the U6 number thats more accurate. I've included a few charts below showing not only the unemployment, but the shortening of hours worked/worker as well.. these are bad trends in an economy built upon consumer spending:

http://theautomaticearth.blogspot.com/2009/11/november-8-2009-jobs-doom-loop.html

http://www.ritholtz.com/blog/wp-content/uploads/2009/11/weekly_hours-worked-110609.png

{kind=link}

http://www.ritholtz.com/blog/wp-content/uploads/2009/11/unemployment-october-1948-2009.JPG

{kind=link}

There was a nugget of good news in there.. the gains in temp work. That is a leading indicator, though it must be said it's the holiday season and this might be a factor in temp hiring.

Next up on bloc is consumer credit.. this figure went down, and badly. However many dollars are being printed, they're not being lent out to you and me; as I alluded to earlier, they're sitting in bank vaults to cover bad loans. Worse, it appears to be accelerating as for the third quarter the rate of decline is 6%, but in September it was 7.25%. This should strengthen the USD (and my PSTIX) Here's todays numbers:

"Consumer credit decreased at an annual rate of 6 percent in the third quarter of 2009. Revolving credit decreased at an annual rate of 10 percent, and nonrevolving credit decreased at an annual rate of 3-3/4 percent. In September, consumer credit decreased at an annual rate of 7-1/4 percent"

http://market-ticker.denninger.net/uploads/Nov2009/credit.png

{kind=link}

Remember, the US economy is 70% consumption.. and if people are not working, if those who are working are working less hours, and they have less and less available credit, who will do the consuming ?? This is Exhibit A on why I believe all is not well, why I think a bout of deflation is coming, and behind it all is the mountain of debt we're still in, a decent part of which is guaranteed by the taxpayers. I caught this little blurb on the article which says Freddie Mac lost another $5 billion last month:

"Starting in 2010, Freddie Mac will begin accounting for $1.8 trillion in mortgage-backed securities it guarantees on its balance sheet to meet new guidelines. This will increase interest income and interest expenses, and could have a significant negative impact on net worth, it said"

Who backs up Freddie Mac and that $1.8 trillion ?? Yep.. us taxpayers. It's "heads I win, tails you lose" in the housing markets these days.

CitiGroup is (again) in trouble, and with the rumblings in Wash DC to break up the "too big to fails", I'm beginning to think that Citi might be the first patient on the operating table. There are parts of Citi that are gems.. but as a whole, they went so deep into subprime mortgages that overall it's toast:

http://www.nytimes.com/2009/11/01/business/economy/01citi.html

Thursday, November 5, 2009

more Muni Bonds

"Nov. 5 (Bloomberg) -- U.S. state and local government pensions are underfunded by $1 trillion and may need to seek federal guarantees for their debt, according to Orin Kramer, chairman of New Jersey’s Investment Council.

Pension underfunding eventually will make it impossible for some governments to raise money in bond markets and will require federal intervention through explicit or “implied guarantees” of municipal debt, Kramer, 64, said in an interview today at Bloomberg News headquarters in New York.

“The collective deficits should not be and will not be overcome by an aggressive investment strategy,” Kramer said. “I think that actually, ultimately, the severity of the problem will become publicly visible and you’ll have more entities that will have difficulty accessing the bond markets.”

The 100 largest U.S. public-employee pension plans had assets of $2.2 trillion as of June 30, down from $2.8 trillion a year earlier, according to a U.S. Census Bureau report. The 21 percent decline compared with the 28 percent fall in the Standard & Poor’s 500 Index during the worst recession since the Great Depression"

It's possible that Uncle Sam will use the already broke FDIC to back up this mega mess. The FDIC has a $500 billion backstop from the Fed, and between bank failures, muni failures and other failures, may need every dime of it. Someone has to pick up the pieces.. and yes, it's us.

In other news, the equities markets continue to rise.. along with unemployment and reduced consumer spending. It has something to do with the USD "carry trade", which makes it easy for banks and others to get loans from the Fed at near zero rates and then gamble them on the stock markets. Roubini had an article about this, saying that there is a danger that should the USD begin to strengthen again, a huge whipsaw effect could bring about severe deflation. In addition, Bernanke seems determined to keep the USD weak to avoid deflation. At some point, all stock market bubbles burst if not supported by the facts on the ground..

In other news, Fannie Mae needs another $15 billion dollars from Bernanke. FNM's loss for Q3 is $18.9 billion, up from $14.8 billion in Q2.

There are rumors that Uncle Sam wants to break apart the "too big to fail" banks.. they'll need to be careful how it's done so as to not trigger a stockholder stampede out the backdoor and thus trigger credit default swaps.

Pension underfunding eventually will make it impossible for some governments to raise money in bond markets and will require federal intervention through explicit or “implied guarantees” of municipal debt, Kramer, 64, said in an interview today at Bloomberg News headquarters in New York.

“The collective deficits should not be and will not be overcome by an aggressive investment strategy,” Kramer said. “I think that actually, ultimately, the severity of the problem will become publicly visible and you’ll have more entities that will have difficulty accessing the bond markets.”

The 100 largest U.S. public-employee pension plans had assets of $2.2 trillion as of June 30, down from $2.8 trillion a year earlier, according to a U.S. Census Bureau report. The 21 percent decline compared with the 28 percent fall in the Standard & Poor’s 500 Index during the worst recession since the Great Depression"

It's possible that Uncle Sam will use the already broke FDIC to back up this mega mess. The FDIC has a $500 billion backstop from the Fed, and between bank failures, muni failures and other failures, may need every dime of it. Someone has to pick up the pieces.. and yes, it's us.

In other news, the equities markets continue to rise.. along with unemployment and reduced consumer spending. It has something to do with the USD "carry trade", which makes it easy for banks and others to get loans from the Fed at near zero rates and then gamble them on the stock markets. Roubini had an article about this, saying that there is a danger that should the USD begin to strengthen again, a huge whipsaw effect could bring about severe deflation. In addition, Bernanke seems determined to keep the USD weak to avoid deflation. At some point, all stock market bubbles burst if not supported by the facts on the ground..

In other news, Fannie Mae needs another $15 billion dollars from Bernanke. FNM's loss for Q3 is $18.9 billion, up from $14.8 billion in Q2.

There are rumors that Uncle Sam wants to break apart the "too big to fail" banks.. they'll need to be careful how it's done so as to not trigger a stockholder stampede out the backdoor and thus trigger credit default swaps.

Wednesday, November 4, 2009

The Sum of all Fears

In a nutshell, I'll try and explain the reasons why the US economy (and others as well) are in very real danger, though it must be said less danger than last September. For those of you who think this isn't a big deal or that recovery is just around the corner, you're going to be sadly mistaken. There will be no recovery in the USA until we as a nation pay down (and/or bankrupt) the enormous debt we've accumulated. Here's my thesis on what went wrong:

Beginning in the Reagan years, the US began living WAY beyond it's means; for the five decades ending in 1980, the total amount of debt we as a nation were in (US Govt, mortgage, corporate, personal and GSE combined) was always around 150% of our GDP. Starting around 1980, banks abandoned all semblance of common sense and began lending to people who had no business getting loans. When I was a kid in the 1970s, my father complained endlessly about the 20% down requirement for getting a mortgage. Banks, which up to that point were leveraged at ten to one since the 1930's (ten dollars loaned out for every dollar in the vault) began leveraging themselves up and up; by the late 2000s, big banks found that they had leveraged themselves to thirty five and forty to one. (Remember.. if a bank is leveraged at ten to one, and one tenth of their loans go bad, the bank is toast. Forty to one.. only one fortieth). The politicians in Washington were (I believe) simply ignorant of these facts.. Alan Greedspan was telling them that all was well since the late 80s. I knew a gal who was not even employed (no doc loan) and got herself a $200K house with only 3% down !! We as a nation consumed SO MUCH that our economy became 70% consumption and 30% production.. utter madness. As banks become more and more leveraged, they loaned out to riskier and riskier clients.. it was insanity. Worse, nearly all levels of government were doing the same during these boom years.. the US Gov't slowly but surely borrowed $7 trillion+ after Reagan defeated Carter. All of it created the greatest prosperity any nation has ever known. But it was built on a mountain of debt.. our total debt-GDP ratio exploded to 375% of GDP.: http://market-ticker.org/uploads/debt-trend-breakdown_2.jpg The banks, now finding that these loans cannot be paid, are selling most of their assets for cash to cushion their leverage positions (deflation/deleveraging), sucking the cash out of the economy. This is why gas went from $4.29 to $1.99 last year.. less cash in the system as opposed to the goods available for that cash.

Worse, the big banks began writing huge insurance policies (called credit default swaps) on each other and a number of other things, thus making their situation far, far more perilous. Here's my article explaining these exceedingly dangerous devices:

http://themeanoldinvestor.blogspot.com/2009/11/investment-update-unemployment-credit.html

For most people, these big numbers don't mean much and, so far, have not affected them too much, although most do realize there's a tough recession going on. Most have the cavalier attitude that "nothing like that can happen here; this is America". But remember.. the 1920s were called the "Roaring 20's" and much of it was funded by overzealous bank loans to do leveraged stock purchases and consumer loans (sound familiar ?).. and it all ended with the stock market crash in Oct 1929. Remember this.. during the Depression, there was a nice stock market bounce throughout much of 1930 and 1931 (the crash was in October, 1929)... and then came a complete collapse in 1932/33. Here's an article Ambrose did earlier this year.. it's a fabulous read on where we are, and especially fabulous are the stories it tells of the Depression that most of us never knew about: http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/4339501/Bad-news-were-back-to-1931.-Good-news-its-not-1933-yet.html

As for a recovery, it seems that the plan is to print and print more; most of this money is winding up in the stock markets and bank vaults, with little of it going back to the rest of us. I do believe this trend will continue for some time, with the result being that there will be no consumer driven recovery as available credit continues to constrict and unemployment (and under-employment) continues to worsen, never mind that most Americans are still neck deep in debt (or bankrupt). So far, inflation has'nt been a problem, and I doubt it will anytime soon given the low amounts of this money seeing its way back onto Main St. I also don't see much deflation since Bernanke will do whatever it takes to keep that at bay. Unemployment will go to at least 12% next year and hundreds more banks will fail http://www.calculatedriskblog.com/2009/11/unofficial-problem-bank-list-increases.html & the FDIC will need massive aid as the commercial real estate debacle begins and the Alt-A and Option-A mortgage refi mess begins (remember.. to do a refi, the home/commercial property has to be worth at least the amount you want to refinance; a lot are'nt). There will be a second stimulus in 2010, with a lot of this going to municipal governments to prevent a debacle in the muni bond markets. The Fed will also be forced to keep the MBS purchases (scheduled to end next Feb) to help the mortgage markets and perhaps will need to begin purchasing Bonds again. The deficit will again be in the $1.5 trillion range, though there is word that there will be a dandy tax hike on the rich in Pelosi's healthcare bill that will take effect in 2010. I think crude oil will go up, forcing up prices on nearly everything in the US, further weakening consumer spending and hiking credit card default rates. Gold will continue it's march to the stars, hitting at least $1,300 next year. I think equities will be forced lower on the weakness of consumer spending. In other words, there is no recovery at least thru next year, despite the efforts of the stimulus packages. In the US Bond markets, given the amount we are going to need to borrow (and the amount others will need to borrow as well) and that the Fed is no longer purchasing, there is a chance rates will rise, and along with this go the mortgage rates, with predictable results. While the US can weather a 2-3% hike in rates, Japan cannot (see article below). The muni bond market will likely be OK for the most part if there is a second stimulus, though rates for some will continue to spiral. Bernanke knows the danger spiking interest rates present and so will be very agressive in preventing such.

There are today some nations living the nightmare already; Spain's unemployment is 20%; Greece, Ireland, Latvia and Iceland are in Depressions as well. Next up on the plank will be England and Japan, who's economies are in worse shape than ours is.

Other nations, in particular Japan and European Union countries, also have very serious economic issues. EU banks, not to be outdone by Yankee banks, have leveraged themselves to heights far above ours.. worse, many of these loans are to third world and former East Bloc nations who's economies and currencies are a mess and have a high chance of defaulting (US banks mostly loaned to American consumers and companies). For example, Austrian banks loaned hundreds of billions to citizens of eastern europe to buy houses; the loans were written in Euros, not the local currencies; when the crisis came, the local currencies went to pot and so instead of a mortgage note of, say, 500 zlotys (the Polish currency) a month, it now cost 700 zlotys. Default rates soared. In the case of Japan, this outstanding article sums it up nicely: http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/6480289/It-is-Japan-we-should-be-worrying-about-not-America.html

The world's economy is highly integrated; what affects one nation will affect others, thanks in no small part to the invention of the credit default swap. With so many nations in such trouble, the world's economy is very delicate. One major problem could send us all off the plank, though it's strong enough to weather small problems (Iceland, Latvia etc). Here is an article from Hong Hong's governor on what the US printing will do to other nations (create bubbles): http://www.bloomberg.com/apps/news?pid=newsarchive&sid=aU3AiTc_Q_vk

How bad can it get ?? Here's a video of Congressman Kanjorski of Ohio, who sits on the House Financial Services Committee and the Capital Markets Subcommittee, on what went down last September.. this is The Sum of all Fears: http://www.youtube.com/watch?v=HOhc2e6UfMM

This is all going to end very badly, and it will happen very quick when it does. I think there's a good chance the next crash will start in another nation, with Japan (their bond market) and Europe (their banks, sovereign debt) at the head of this. A war and/or serious terrorist attack could trigger this, especially if crude prices are above $125 for an extended period. I do not see us getting into 2012 before another crash occurs in one form or another. But with equal measures of resourcefulness, hard work and frugality, working together, this too shall pass. Lets up hope that after this baby goes down we as a nation will see fit not to burden our own children with trillions in debt and give too much power to Gov't, who is either incapable or willfully ignorant of the catastrophe they are allowing and participating in.

Beginning in the Reagan years, the US began living WAY beyond it's means; for the five decades ending in 1980, the total amount of debt we as a nation were in (US Govt, mortgage, corporate, personal and GSE combined) was always around 150% of our GDP. Starting around 1980, banks abandoned all semblance of common sense and began lending to people who had no business getting loans. When I was a kid in the 1970s, my father complained endlessly about the 20% down requirement for getting a mortgage. Banks, which up to that point were leveraged at ten to one since the 1930's (ten dollars loaned out for every dollar in the vault) began leveraging themselves up and up; by the late 2000s, big banks found that they had leveraged themselves to thirty five and forty to one. (Remember.. if a bank is leveraged at ten to one, and one tenth of their loans go bad, the bank is toast. Forty to one.. only one fortieth). The politicians in Washington were (I believe) simply ignorant of these facts.. Alan Greedspan was telling them that all was well since the late 80s. I knew a gal who was not even employed (no doc loan) and got herself a $200K house with only 3% down !! We as a nation consumed SO MUCH that our economy became 70% consumption and 30% production.. utter madness. As banks become more and more leveraged, they loaned out to riskier and riskier clients.. it was insanity. Worse, nearly all levels of government were doing the same during these boom years.. the US Gov't slowly but surely borrowed $7 trillion+ after Reagan defeated Carter. All of it created the greatest prosperity any nation has ever known. But it was built on a mountain of debt.. our total debt-GDP ratio exploded to 375% of GDP.: http://market-ticker.org/uploads/debt-trend-breakdown_2.jpg The banks, now finding that these loans cannot be paid, are selling most of their assets for cash to cushion their leverage positions (deflation/deleveraging), sucking the cash out of the economy. This is why gas went from $4.29 to $1.99 last year.. less cash in the system as opposed to the goods available for that cash.

{kind=link}

Worse, the big banks began writing huge insurance policies (called credit default swaps) on each other and a number of other things, thus making their situation far, far more perilous. Here's my article explaining these exceedingly dangerous devices:

http://themeanoldinvestor.blogspot.com/2009/11/investment-update-unemployment-credit.html

For most people, these big numbers don't mean much and, so far, have not affected them too much, although most do realize there's a tough recession going on. Most have the cavalier attitude that "nothing like that can happen here; this is America". But remember.. the 1920s were called the "Roaring 20's" and much of it was funded by overzealous bank loans to do leveraged stock purchases and consumer loans (sound familiar ?).. and it all ended with the stock market crash in Oct 1929. Remember this.. during the Depression, there was a nice stock market bounce throughout much of 1930 and 1931 (the crash was in October, 1929)... and then came a complete collapse in 1932/33. Here's an article Ambrose did earlier this year.. it's a fabulous read on where we are, and especially fabulous are the stories it tells of the Depression that most of us never knew about: http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/4339501/Bad-news-were-back-to-1931.-Good-news-its-not-1933-yet.html

As for a recovery, it seems that the plan is to print and print more; most of this money is winding up in the stock markets and bank vaults, with little of it going back to the rest of us. I do believe this trend will continue for some time, with the result being that there will be no consumer driven recovery as available credit continues to constrict and unemployment (and under-employment) continues to worsen, never mind that most Americans are still neck deep in debt (or bankrupt). So far, inflation has'nt been a problem, and I doubt it will anytime soon given the low amounts of this money seeing its way back onto Main St. I also don't see much deflation since Bernanke will do whatever it takes to keep that at bay. Unemployment will go to at least 12% next year and hundreds more banks will fail http://www.calculatedriskblog.com/2009/11/unofficial-problem-bank-list-increases.html & the FDIC will need massive aid as the commercial real estate debacle begins and the Alt-A and Option-A mortgage refi mess begins (remember.. to do a refi, the home/commercial property has to be worth at least the amount you want to refinance; a lot are'nt). There will be a second stimulus in 2010, with a lot of this going to municipal governments to prevent a debacle in the muni bond markets. The Fed will also be forced to keep the MBS purchases (scheduled to end next Feb) to help the mortgage markets and perhaps will need to begin purchasing Bonds again. The deficit will again be in the $1.5 trillion range, though there is word that there will be a dandy tax hike on the rich in Pelosi's healthcare bill that will take effect in 2010. I think crude oil will go up, forcing up prices on nearly everything in the US, further weakening consumer spending and hiking credit card default rates. Gold will continue it's march to the stars, hitting at least $1,300 next year. I think equities will be forced lower on the weakness of consumer spending. In other words, there is no recovery at least thru next year, despite the efforts of the stimulus packages. In the US Bond markets, given the amount we are going to need to borrow (and the amount others will need to borrow as well) and that the Fed is no longer purchasing, there is a chance rates will rise, and along with this go the mortgage rates, with predictable results. While the US can weather a 2-3% hike in rates, Japan cannot (see article below). The muni bond market will likely be OK for the most part if there is a second stimulus, though rates for some will continue to spiral. Bernanke knows the danger spiking interest rates present and so will be very agressive in preventing such.

There are today some nations living the nightmare already; Spain's unemployment is 20%; Greece, Ireland, Latvia and Iceland are in Depressions as well. Next up on the plank will be England and Japan, who's economies are in worse shape than ours is.

Other nations, in particular Japan and European Union countries, also have very serious economic issues. EU banks, not to be outdone by Yankee banks, have leveraged themselves to heights far above ours.. worse, many of these loans are to third world and former East Bloc nations who's economies and currencies are a mess and have a high chance of defaulting (US banks mostly loaned to American consumers and companies). For example, Austrian banks loaned hundreds of billions to citizens of eastern europe to buy houses; the loans were written in Euros, not the local currencies; when the crisis came, the local currencies went to pot and so instead of a mortgage note of, say, 500 zlotys (the Polish currency) a month, it now cost 700 zlotys. Default rates soared. In the case of Japan, this outstanding article sums it up nicely: http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/6480289/It-is-Japan-we-should-be-worrying-about-not-America.html

The world's economy is highly integrated; what affects one nation will affect others, thanks in no small part to the invention of the credit default swap. With so many nations in such trouble, the world's economy is very delicate. One major problem could send us all off the plank, though it's strong enough to weather small problems (Iceland, Latvia etc). Here is an article from Hong Hong's governor on what the US printing will do to other nations (create bubbles): http://www.bloomberg.com/apps/news?pid=newsarchive&sid=aU3AiTc_Q_vk

How bad can it get ?? Here's a video of Congressman Kanjorski of Ohio, who sits on the House Financial Services Committee and the Capital Markets Subcommittee, on what went down last September.. this is The Sum of all Fears: http://www.youtube.com/watch?v=HOhc2e6UfMM

This is all going to end very badly, and it will happen very quick when it does. I think there's a good chance the next crash will start in another nation, with Japan (their bond market) and Europe (their banks, sovereign debt) at the head of this. A war and/or serious terrorist attack could trigger this, especially if crude prices are above $125 for an extended period. I do not see us getting into 2012 before another crash occurs in one form or another. But with equal measures of resourcefulness, hard work and frugality, working together, this too shall pass. Lets up hope that after this baby goes down we as a nation will see fit not to burden our own children with trillions in debt and give too much power to Gov't, who is either incapable or willfully ignorant of the catastrophe they are allowing and participating in.

Tuesday, November 3, 2009

The Problem with Muni Bonds

The $3 trillion muni bond market.. where state, city and county governments borrow money.. looks to be in some trouble, though probably not too serious yet. Here's a summary of the problem:

http://www.ritholtz.com/blog/2009/11/state-local-taxes-plummet/

* Many states and cities have had their tax base crushed in the last year; New York and California saw revenues drop 20-25%, with lesser drops nearly everywhere in between. Some cities got it even worse.. imagine being the financial chief for the city of Detroit these days. On the county level (in most cases) a significant part of the tax revenue comes from property taxes.. and in most cases, this is falling as property value plummets and foreclosures bring fewer and fewer property tax payers. Whoops.

* As part of the economic stimulus of 2009, local governments got about $50 billion in aid from Uncle Sam. This won't happen again next year.

* As the economy got worse, the demand for social services (food stamps, medical assistance, welfare etc) grew expotentially.

* Many of these governments had invested in the stock market as a way to earn money and pay bills and/or retirees (CalPers). This year isn't too bad with the stock market rally; last year was brutal.

* Many of these governments were running deficits during the good years of the 1990s and 2000s, thinking that the good times would never really end and/or that if debt became a problem, it was a problem for the dude elected after I left.

Under these circumstances, the fear that a city or county will simply say "sorry dude.. not this year" and default is higher than ever.. and muni bond markets are pricing this risk accordingly, cruelly making the problem even worse as they charge higher rates. So far not too much higher, but the rates are creeping up, especially for those municipalities who are deeply in debt or who have been hit hardest by the downturn.

Recently the city of Vallejo, CA filed bankruptcy.. this will be a test case. During the Depression, municipalities initially were not allowed to file banko.. with the results being property tax hikes to unimaginable levels.. West Palm Beach had property taxes at 42.5% of assessed value. It was insanity, and eventually they were allowed to file bankruptcy, allowing a mad rush to the bankruptcy courthouses.

Today its a little more complex.. for example, who has the highest claim to what is left of Vallejo CA.. retirees or bondholders ?? Remember that when GM and Chrysler went under, the Obama Administration rose up for their union buddies and gave the bondholders (who had legal claim to first rights on whats left of the company) the shaft. Should this be how it shakes down in Vallejo, look for muni bond rates, especially for those deemed in trouble, to spike up nicely; some cities might not even be able to get anyone to buy them.

Remember that it's a $3 trillion dollar market.. the Vallejo case is important for those reasons. If Vallejo goes under without any real consequences, what would prevent a hundred other cities from doing the same ??

Here's a good article on this mess:

http://blogs.law.harvard.edu/philg/2009/11/03/the-coming-collapse-of-the-municipal-bond-market/

Here's the latest from Vallejo:

http://www.vallejobankruptcyupdate.com/

My impression overall here is that this mess is completely unnoticed.. everyone is concerned with the stock market, unemployment, housing, the USD, gold.. and if my hunch of deflation is correct, municipalities will have a very hard time finding buyers for their bonds at decent rates. The Vallejo case is important to watch. This is a HUGE market folks..

http://www.ritholtz.com/blog/2009/11/state-local-taxes-plummet/

* Many states and cities have had their tax base crushed in the last year; New York and California saw revenues drop 20-25%, with lesser drops nearly everywhere in between. Some cities got it even worse.. imagine being the financial chief for the city of Detroit these days. On the county level (in most cases) a significant part of the tax revenue comes from property taxes.. and in most cases, this is falling as property value plummets and foreclosures bring fewer and fewer property tax payers. Whoops.

* As part of the economic stimulus of 2009, local governments got about $50 billion in aid from Uncle Sam. This won't happen again next year.

* As the economy got worse, the demand for social services (food stamps, medical assistance, welfare etc) grew expotentially.

* Many of these governments had invested in the stock market as a way to earn money and pay bills and/or retirees (CalPers). This year isn't too bad with the stock market rally; last year was brutal.

* Many of these governments were running deficits during the good years of the 1990s and 2000s, thinking that the good times would never really end and/or that if debt became a problem, it was a problem for the dude elected after I left.

Under these circumstances, the fear that a city or county will simply say "sorry dude.. not this year" and default is higher than ever.. and muni bond markets are pricing this risk accordingly, cruelly making the problem even worse as they charge higher rates. So far not too much higher, but the rates are creeping up, especially for those municipalities who are deeply in debt or who have been hit hardest by the downturn.

Recently the city of Vallejo, CA filed bankruptcy.. this will be a test case. During the Depression, municipalities initially were not allowed to file banko.. with the results being property tax hikes to unimaginable levels.. West Palm Beach had property taxes at 42.5% of assessed value. It was insanity, and eventually they were allowed to file bankruptcy, allowing a mad rush to the bankruptcy courthouses.

Today its a little more complex.. for example, who has the highest claim to what is left of Vallejo CA.. retirees or bondholders ?? Remember that when GM and Chrysler went under, the Obama Administration rose up for their union buddies and gave the bondholders (who had legal claim to first rights on whats left of the company) the shaft. Should this be how it shakes down in Vallejo, look for muni bond rates, especially for those deemed in trouble, to spike up nicely; some cities might not even be able to get anyone to buy them.

Remember that it's a $3 trillion dollar market.. the Vallejo case is important for those reasons. If Vallejo goes under without any real consequences, what would prevent a hundred other cities from doing the same ??

Here's a good article on this mess:

http://blogs.law.harvard.edu/philg/2009/11/03/the-coming-collapse-of-the-municipal-bond-market/

Here's the latest from Vallejo:

http://www.vallejobankruptcyupdate.com/

My impression overall here is that this mess is completely unnoticed.. everyone is concerned with the stock market, unemployment, housing, the USD, gold.. and if my hunch of deflation is correct, municipalities will have a very hard time finding buyers for their bonds at decent rates. The Vallejo case is important to watch. This is a HUGE market folks..

The Problem with US Bonds

Just a few factoids on who it is that's loaning Uncle Sam all the money Uncle Obama is spending:

* The US Gov't spends three dollars for every two dollars it collects in tax revenues in 2009, and likely at least through 2010.

* "The Q2 Flow of Funds Report published by the Federal Reserve revealed that the Federal Reserve purchased as much as half of the newly issued Treasuries in the second quarter" (What this means is that the Fed printed about $180 billion out of thin air and "loaned it" to Uncle Sam)

* "According to reports, in the red flag category, US treasury holdings of China came down from $800 billion to $797 billion. In August China was a net seller of $3.3 billion" (The Chinese are selling more Bonds than they're buying)

* Foreign nations purchase roughly half of the Bonds we issue. Fellow Americans only purchase about 10%. The rest get "bought" by the Fed.

* This recession (well, depression really) has hit other nations as well, and their governments are doing much the same as ours is.. borrowing like there's no tomorrow, because of they don't, there would'nt be a tomorrow for those elected officials.

* This depression has also hit local governments.. state, county, cities.. in the wallet. They, too, are borrowing money via Muni Bonds, which I'll get to in a later post.

* As the assets on the US balance sheet become increasingly long-dated, courtesy of QE, and locking in record low rates, US liabilities in turn have shortened their duration to a record level. Almost $3 trillion in US debt will have to be rolled by the end of 2010. But wait, that's just the existing debt that has to be rolled over. Then there's the new debt that has to be added to keep things rolling along: Porter Stansberry estimates the US government alone will need to finance $4.5 trillion worth of bonds next year, of which $1.5 trillion will be new debt: http://seekingalpha.com/article/174910-deficits-and-massive-debt-overhangs-do-matter

There is only so much money in the world..

Soon enough, we as a nation are going to be forced to live within our means, because its certainly not going to happen willingly.

A few nations are living this out today.

Here's a sneak peek at whats happening to Ireland & Latvia today, the UK & Japan tomorrow, and the US soon thereafter

http://www.telegraph.co.uk/finance/comment/edmundconway/6332695/How-bad-will-spending-cuts-get-Take-a-look-at-Latvia.html

* The US Gov't spends three dollars for every two dollars it collects in tax revenues in 2009, and likely at least through 2010.

* "The Q2 Flow of Funds Report published by the Federal Reserve revealed that the Federal Reserve purchased as much as half of the newly issued Treasuries in the second quarter" (What this means is that the Fed printed about $180 billion out of thin air and "loaned it" to Uncle Sam)

* "According to reports, in the red flag category, US treasury holdings of China came down from $800 billion to $797 billion. In August China was a net seller of $3.3 billion" (The Chinese are selling more Bonds than they're buying)

* Foreign nations purchase roughly half of the Bonds we issue. Fellow Americans only purchase about 10%. The rest get "bought" by the Fed.

* This recession (well, depression really) has hit other nations as well, and their governments are doing much the same as ours is.. borrowing like there's no tomorrow, because of they don't, there would'nt be a tomorrow for those elected officials.

* This depression has also hit local governments.. state, county, cities.. in the wallet. They, too, are borrowing money via Muni Bonds, which I'll get to in a later post.

* As the assets on the US balance sheet become increasingly long-dated, courtesy of QE, and locking in record low rates, US liabilities in turn have shortened their duration to a record level. Almost $3 trillion in US debt will have to be rolled by the end of 2010. But wait, that's just the existing debt that has to be rolled over. Then there's the new debt that has to be added to keep things rolling along: Porter Stansberry estimates the US government alone will need to finance $4.5 trillion worth of bonds next year, of which $1.5 trillion will be new debt: http://seekingalpha.com/article/174910-deficits-and-massive-debt-overhangs-do-matter

There is only so much money in the world..

Soon enough, we as a nation are going to be forced to live within our means, because its certainly not going to happen willingly.

A few nations are living this out today.

Here's a sneak peek at whats happening to Ireland & Latvia today, the UK & Japan tomorrow, and the US soon thereafter

http://www.telegraph.co.uk/finance/comment/edmundconway/6332695/How-bad-will-spending-cuts-get-Take-a-look-at-Latvia.html

In the beginning..

Thanks for stopping by !! This blog is about the worsening macroeconomic news of the world and exactly what I'm doing with an imaginary $10,000 trading account to see if I'm actually any good at this. I'll be posting what I'm investing in (and why), results on a weekly (or so) basis, as well as some news here and there and how I think it might affect your investments.

Today I'll start by putting 100% of my $10K into Pimco's Bear Fund (PSTIX) which is heavily cash and Gov't bonds. It's at 5.55 today. The reason is that I'm expecting a little deflation (USDX is at 76.2) and for the equities markets to go down some (DOW is at 9775). The recent M3 money chart from shadowstats shows that while the overall M2 money supply is still going up, the velocity of money is sinking, making it harder for the average US consumer to get loans. The banks are taking a beating on bad loans and are still hoarding cash to cushion the blow of the bad loans, thus making available cash more valueable. I see gold and crude going down, or at best sideways, despite today's high in gold. I simply can't see how equities can rally from these levels without better fundamentals, although I must say that yesterday's manufacturing numbers were actually quite impressive.

Here's a link to an article on deflation:

http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/6448884/Deflation-fears-as-Eurozone-and-US-credit-contracts.html

Yesterday Ambrose Evans-Pritchard published an excellent article of the state of the Japanese economy that was truly scary. It describes a nation helplessly drifting into default, and most scary of all is that the credit default swap markets agree.. it's now three times as expensive to insure Japanese Gov't debt as it is to insure US Gov't debt. Unless something changes there, and soon, the Bond vigilantes will force a Depression-era cuts in basic services and social security, much like Ireland and Iceland has had to endure, only with less hope for the future as Japan is an aging society with fewer and fewer workers:

http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/6480289/It-is-Japan-we-should-be-worrying-about-not-America.html

Also remember that Japan is the second largest holders of US bonds, and if they came to a serious crunch, would have to liquidate their US assets to prop up their finances back home by cashing in their short term US treasuries instead of rolling them over as most investors do. This has the potential to blow a nice hole in the port bow of the USS Uncle Sam should it occur. As far as I can see, this appears to be the most serious problem facing the world economy.. at the moment.

Disclaimer: This should not be construed as investment advice. Any investment involves the possibility of loss.

Today I'll start by putting 100% of my $10K into Pimco's Bear Fund (PSTIX) which is heavily cash and Gov't bonds. It's at 5.55 today. The reason is that I'm expecting a little deflation (USDX is at 76.2) and for the equities markets to go down some (DOW is at 9775). The recent M3 money chart from shadowstats shows that while the overall M2 money supply is still going up, the velocity of money is sinking, making it harder for the average US consumer to get loans. The banks are taking a beating on bad loans and are still hoarding cash to cushion the blow of the bad loans, thus making available cash more valueable. I see gold and crude going down, or at best sideways, despite today's high in gold. I simply can't see how equities can rally from these levels without better fundamentals, although I must say that yesterday's manufacturing numbers were actually quite impressive.

Here's a link to an article on deflation:

http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/6448884/Deflation-fears-as-Eurozone-and-US-credit-contracts.html

Yesterday Ambrose Evans-Pritchard published an excellent article of the state of the Japanese economy that was truly scary. It describes a nation helplessly drifting into default, and most scary of all is that the credit default swap markets agree.. it's now three times as expensive to insure Japanese Gov't debt as it is to insure US Gov't debt. Unless something changes there, and soon, the Bond vigilantes will force a Depression-era cuts in basic services and social security, much like Ireland and Iceland has had to endure, only with less hope for the future as Japan is an aging society with fewer and fewer workers:

http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/6480289/It-is-Japan-we-should-be-worrying-about-not-America.html

Also remember that Japan is the second largest holders of US bonds, and if they came to a serious crunch, would have to liquidate their US assets to prop up their finances back home by cashing in their short term US treasuries instead of rolling them over as most investors do. This has the potential to blow a nice hole in the port bow of the USS Uncle Sam should it occur. As far as I can see, this appears to be the most serious problem facing the world economy.. at the moment.

Disclaimer: This should not be construed as investment advice. Any investment involves the possibility of loss.

Subscribe to:

Posts (Atom)